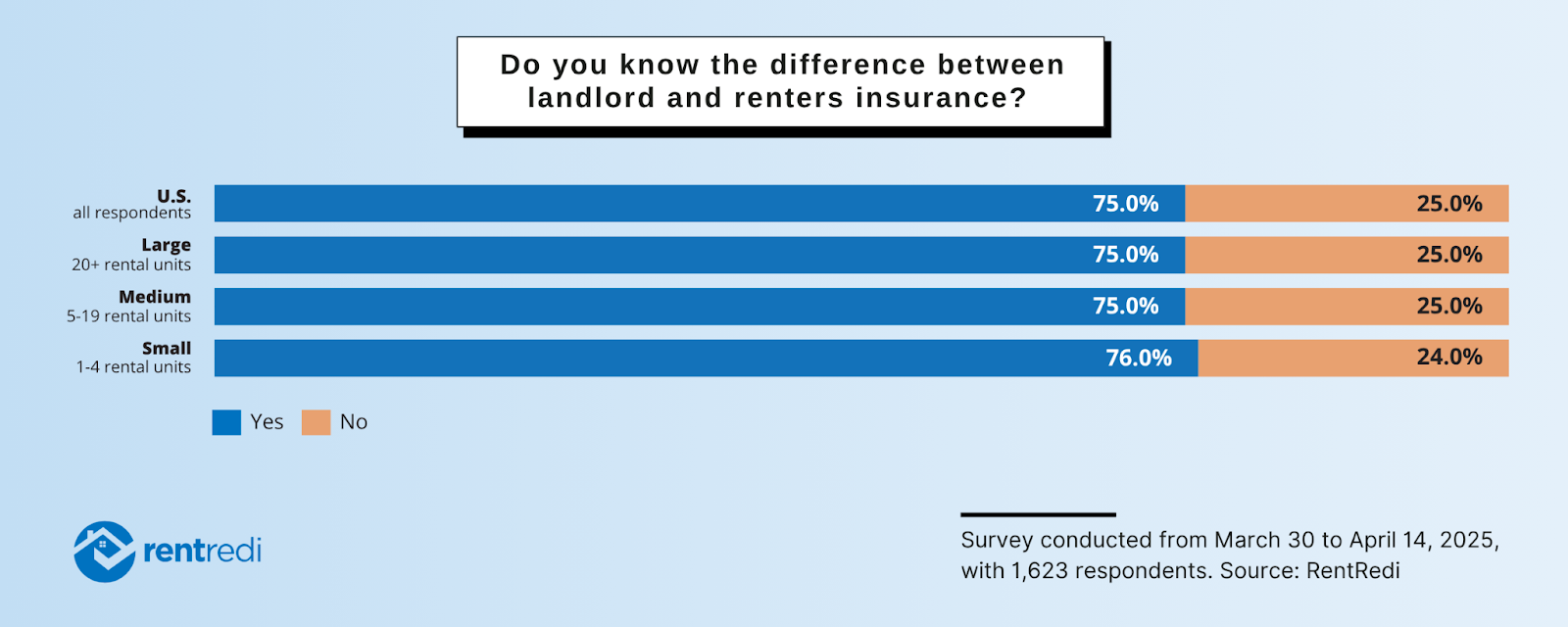

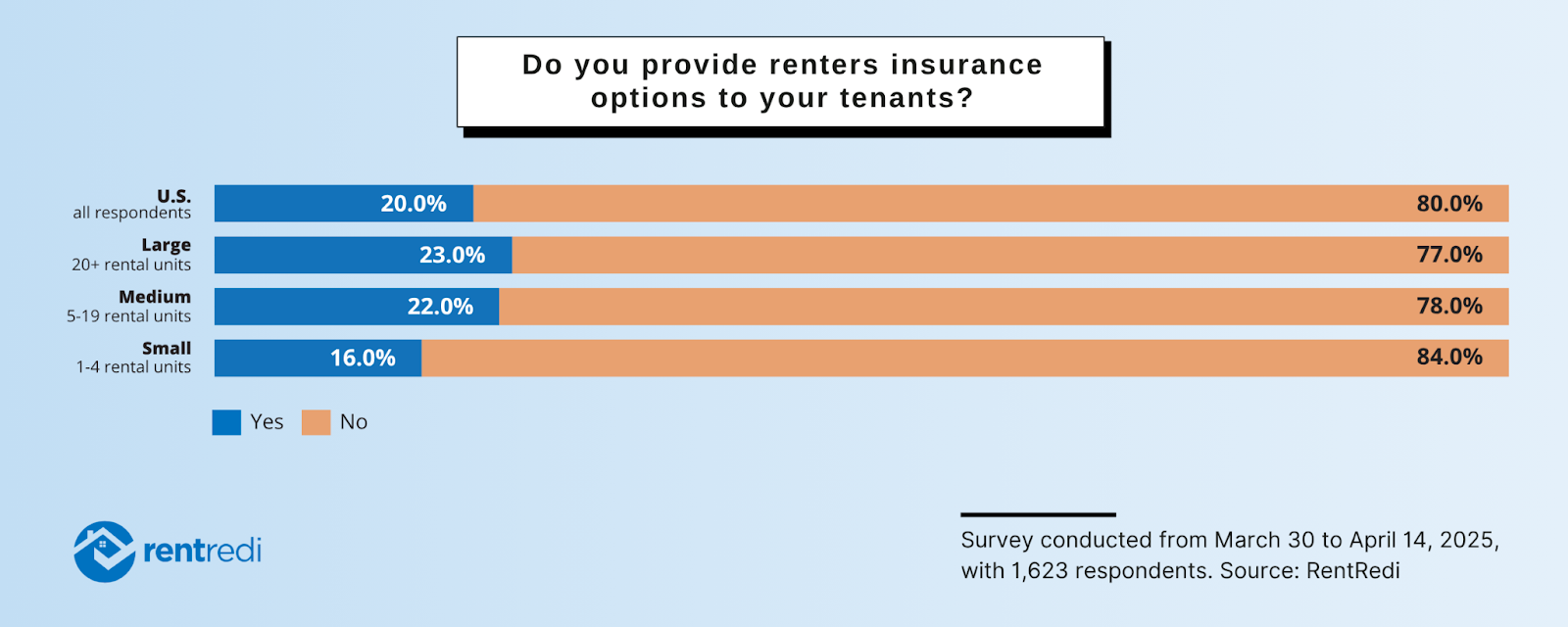

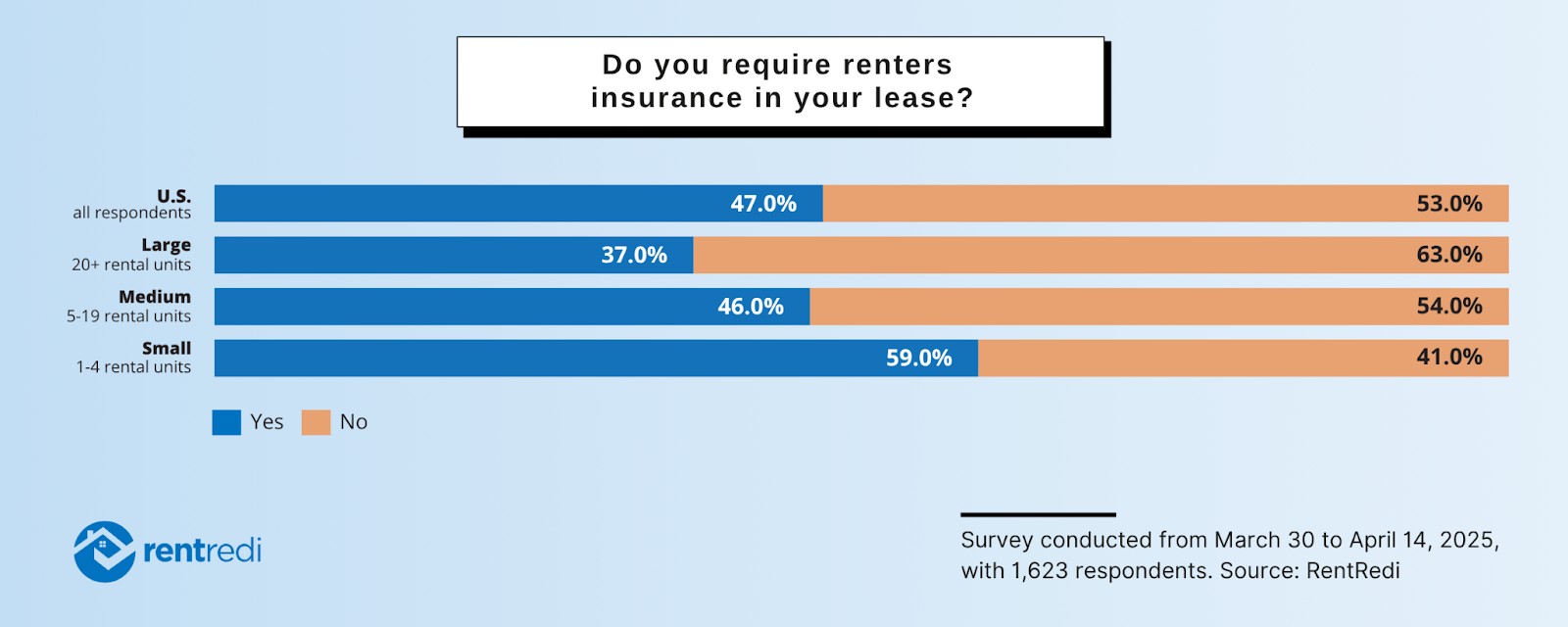

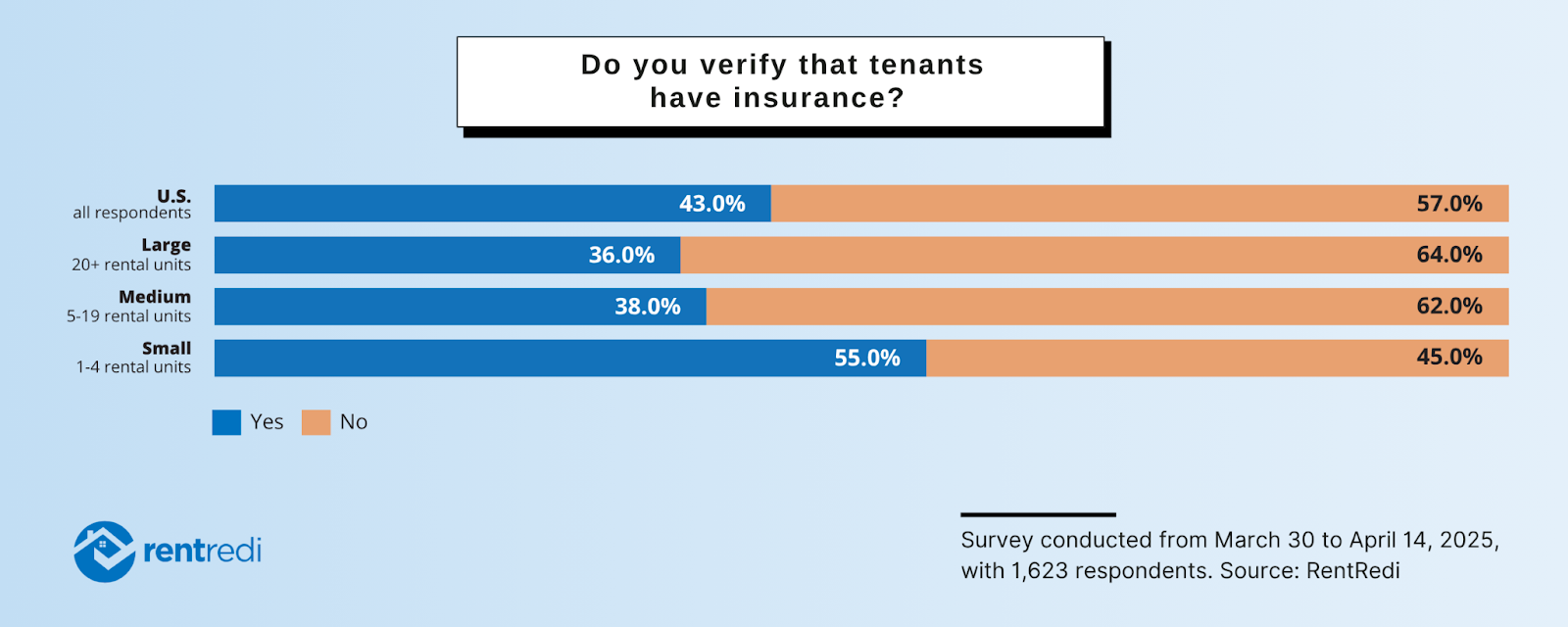

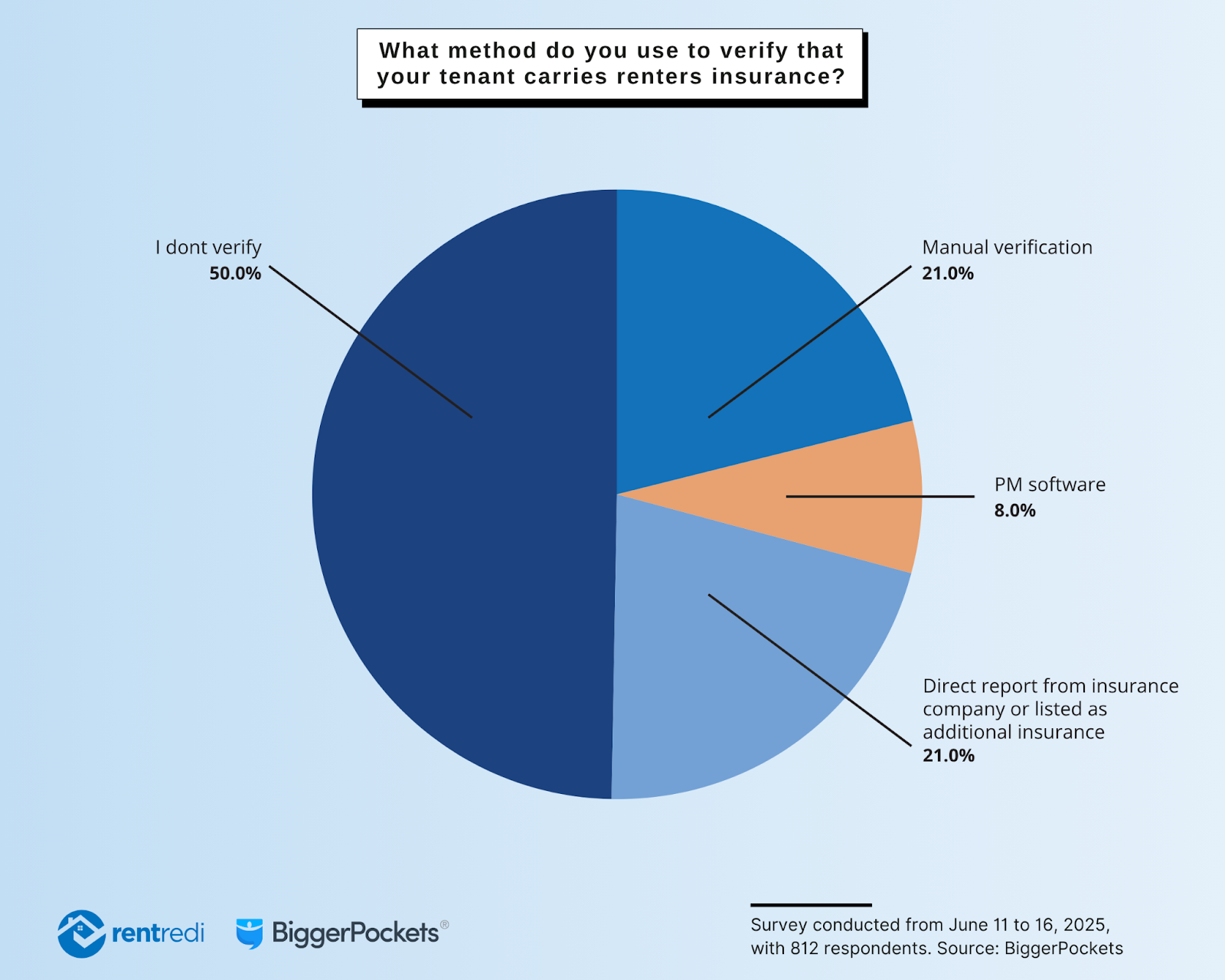

A new renters insurance report from RentRedi and BiggerPockets takes a closer look at how landlords think about, and handle, renters insurance. Most landlords understand the difference between renters insurance and landlord insurance, but many aren’t requiring tenants to have it. Even fewer are taking steps to verify coverage. That gap can leave both landlords and renters exposed to financial risk, especially as rental portfolios grow and things get more complex.

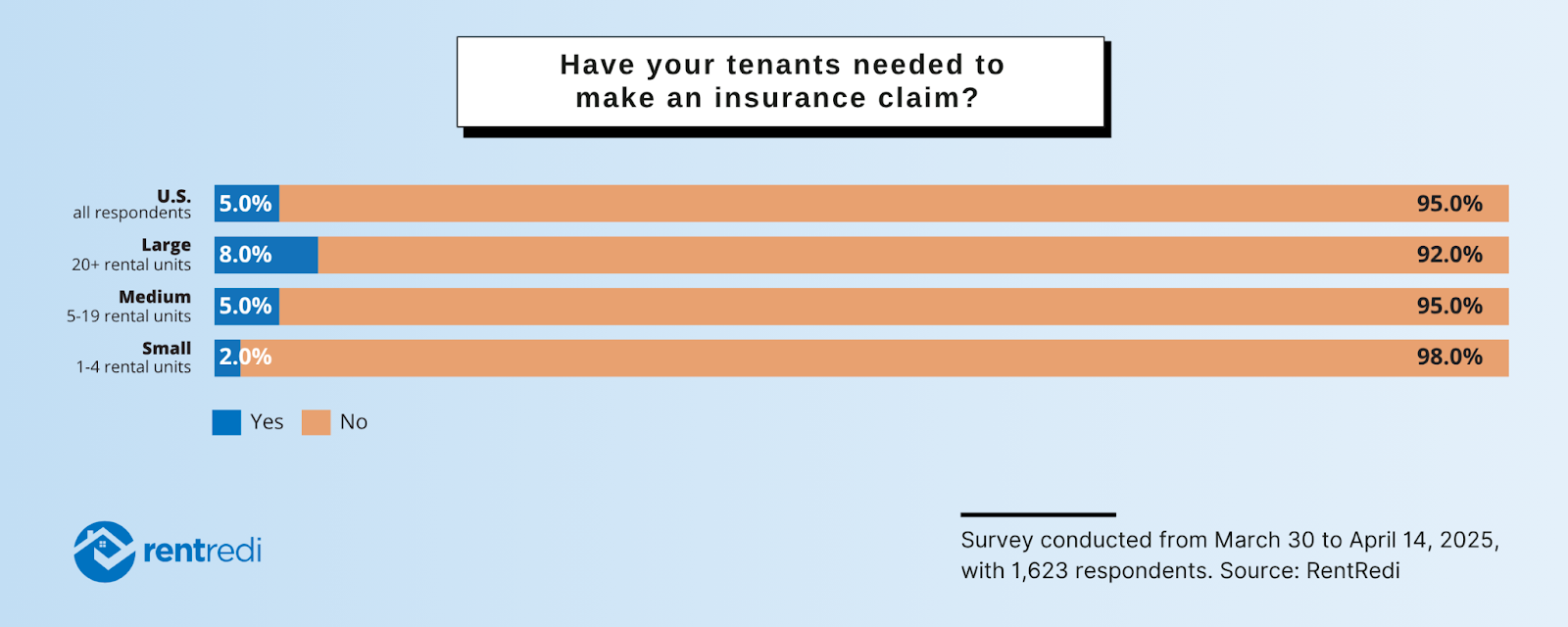

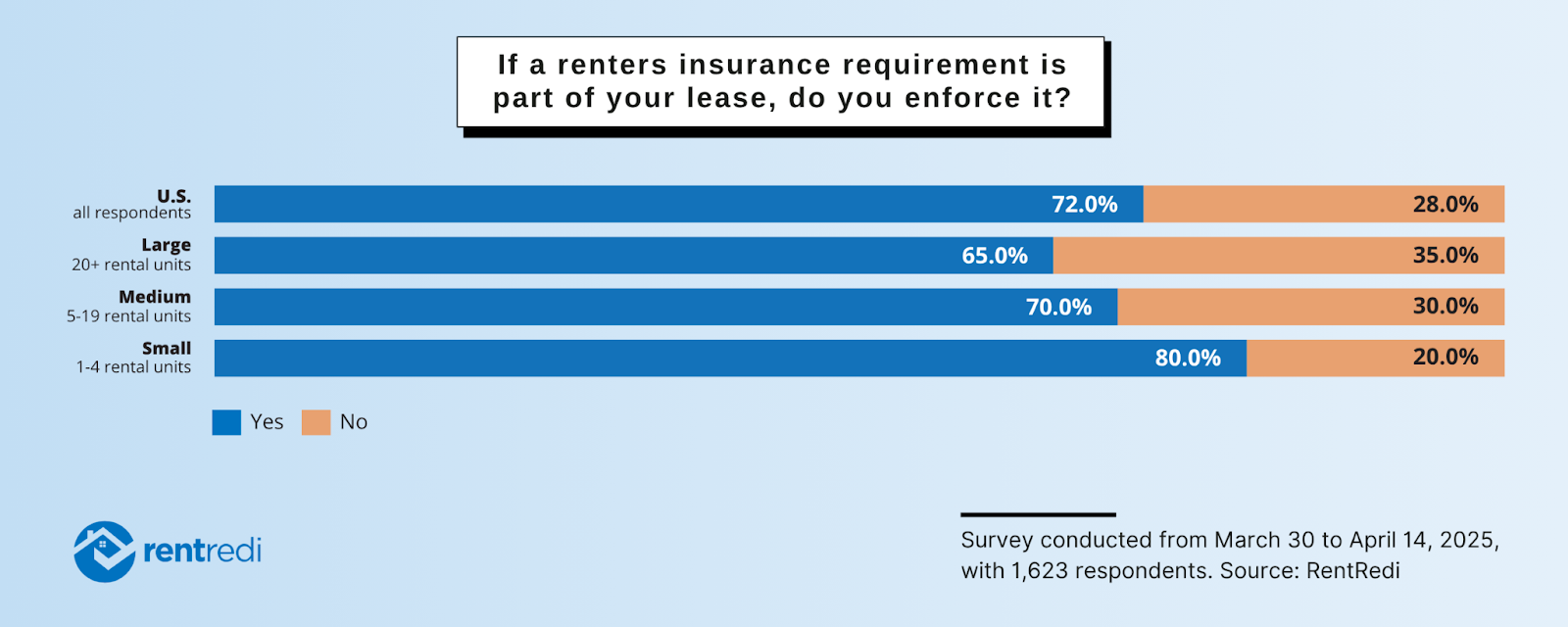

But the data also points to a potential opportunity. Smaller landlords, in particular, are stepping up. Turns out they’re 60% more likely to require renters insurance than landlords with larger portfolios. It’s proof that with the right tools, it’s possible to stay protected without making things harder for you or your tenants. That’s where platforms like RentRedi come in, offering smart, streamlined ways to manage renters’ insurance so landlords can protect their properties while giving tenants a better experience.

Industry Performance and Market Overview

The performance of the renters insurance industry includes key statistics, market size, and general trends expected in 2025. The renters insurance industry is poised for continued growth in 2025, with market penetration reaching approximately 55% of U.S. renters, representing over 60 million policyholders nationwide. The sector’s total value is projected to climb, driven by increased awareness and affordability, with national average premiums hovering around $170 per year. Industry reports highlight robust expansion fueled by both traditional insurers and innovative digital entrants.

Competitive Landscape and External Influences

The renters insurance industry in the United States is shaped by a dynamic competitive landscape and a host of external influences that affect both insurers and policyholders. Market concentration remains moderate, with a handful of major insurance companies holding significant market share. These established players benefit from brand recognition, extensive distribution networks, and economies of scale, making it challenging for smaller entrants to compete on price and coverage options. However, the rise of digital-first insurers and insurtech startups has started to shift the balance, introducing greater competition through innovative products, streamlined digital experiences, and targeted marketing to younger, tech-savvy renters. Newer entrants often focus on niche segments or offer flexible, usage-based policies that appeal to renters seeking convenience and customization.

Barriers to entry in the renters insurance market are substantial, largely due to regulatory requirements, the need for significant capital reserves, and the complexities of underwriting and claims management. State-level regulations mandate specific solvency standards, licensing, and consumer protection measures, creating hurdles for new companies. Additionally, the regulatory environment is evolving, with some states considering or enacting legislation that influences policy requirements, transparency, and consumer rights. For example, while renters insurance is not required by law at the federal or state level, landlords in many regions are increasingly including it as a lease condition, further driving demand and shaping competitive strategies.

External economic factors also play a pivotal role in shaping the industry. Macroeconomic conditions, such as inflation, employment rates, and housing market trends, directly impact renters’ ability to afford insurance and the overall demand for rental properties. Periods of economic uncertainty may lead to higher claims frequencies or shifts in coverage preferences, compelling insurers to adjust pricing and underwriting standards. Natural disasters and climate-related risks also exert upward pressure on premiums, especially in high-risk states like Mississippi, Louisiana, and Texas, where average annual premiums are typically higher. Insurers must continually assess and price these risks, balancing consumer affordability with the need to maintain profitability.

Furthermore, the competitive landscape is influenced by the growing adoption of technology and the integration of digital tools in policy management and claims processing. Established insurers and newcomers alike are investing in AI-driven personalization, mobile platforms, and automated underwriting to enhance the customer experience and differentiate themselves in a crowded market. As regulatory scrutiny on data privacy and cybersecurity increases, companies must also ensure robust safeguards to protect sensitive customer information.

Demographic and Geographic Disparities

Renters insurance coverage is unevenly distributed across both demographic groups and geographic regions in the United States. Younger renters, lower-income households, and those in shared living arrangements are significantly less likely to have coverage, often due to misconceptions about cost and a lack of awareness about what renters insurance provides. Geographically, coverage rates are lower in states with higher premiums, where increased natural disaster risks drive up costs. These disparities are further influenced by factors like:

- Property age

- Local economic conditions

- Educational outreach

Renters Insurance Report: Data Trends for 2025

Survey Methodology

The joint survey with BiggerPockets, conducted from June 11–16, 2025, gathered responses from 812 real estate investors and property owners. Separately, RentRedi conducted its own survey from March 30 to April 14, 2025, with 1,623 respondents, which analyzes landlord behavior across portfolio sizes. Respondents were asked about their renters’ insurance practices, including verification methods, lease considerations, and use of property management software. In both surveys, percentages have been rounded to the nearest whole number.

Claims Process and Consumer Experience

Filing a renters insurance claim can be a stressful process, especially during an already difficult time. Understanding the steps involved can make a significant difference for both renters and landlords. Below, we break down the key components of the claims process and share strategies to help ensure a smoother, more positive consumer experience.

- Step-by-Step Claims Process: To file a renters insurance claim, notify your insurance provider as soon as possible after an incident occurs. Gather all necessary documentation, including photos of damages, receipts, and a detailed description of the event. Submit your claim through your insurer’s preferred method, often online or via a mobile app. After submission, an adjuster will review the claim, request additional information if needed, and determine the payout or next steps.

- Documentation Challenges: One of the most common obstacles in the claims process is the need to provide adequate documentation. Many renters struggle to recall or prove ownership of lost or damaged items, especially without a pre-existing home inventory. Creating a simple record, such as a video walkthrough or a folder of receipts, can save valuable time and help maximize claim payouts. Without proper documentation, claims may be delayed or result in lower settlements, making preparation essential.

- Delays and Communication Hurdles: Claims processing can be delayed by incomplete information, high volumes during disaster seasons, or slow responses from claimants and adjusters. Renters may spend hours on hold or waiting for email updates, adding to the frustration of an already stressful situation.

- Strategies to Improve the Consumer Experience: Both renters and insurers can adopt proactive strategies to enhance the claims process. Renters should maintain an up-to-date home inventory, store digital copies of important documents, and familiarize themselves with their policy’s requirements. Insurers can leverage technology, such as mobile claims apps and AI-driven support, to simplify submissions and provide real-time updates. Clear communication and transparency throughout the process further contribute to a more positive consumer experience.

By comprehending the claims process and preparing in advance, renters can minimize stress and maximize their chances of a successful outcome. Renters and landlords benefit from streamlined procedures, clear documentation, and open communication, leading to a better experience when it matters most.

Financial Benchmarks and Industry Data

Understanding the financial health and competitiveness of the renters insurance sector requires a close examination of specific benchmarks and industry data. Below are essential financial and operational indicators used to gauge the sector’s status in 2025:

- Industry Revenue Growth Rate: The annual revenue growth rate measures the sector’s expansion or contraction over time. Tracking year-over-year changes in total premiums collected reveals the industry’s resilience, sensitivity to economic shifts, and potential for future profitability.

- Loss Ratio: The loss ratio compares claims paid out to premiums earned, providing insight into underwriting effectiveness and risk management. A lower loss ratio suggests better profitability, while a higher ratio may indicate increased claims frequency or inadequate pricing.

- Combined Ratio: This metric sums the loss ratio and expense ratio, offering a comprehensive view of overall operational efficiency. A combined ratio below 100% means the industry is operating at a profit, while ratios above 100% signal unprofitable underwriting.

- Average Premium Per Policy: Calculating the average annual or monthly premium per policyholder highlights pricing trends and consumer affordability. This benchmark also reflects how risk factors, such as property location and local disaster frequency, influence premium rates across different regions.

- Market Penetration Rate: The market penetration rate is the percentage of eligible renters with active insurance policies. It’s a critical indicator of industry reach, consumer awareness, and untapped growth potential, especially in underinsured demographic or geographic segments.

- Expense Ratio: The expense ratio measures the proportion of premiums spent on administrative and operational costs. Monitoring this ratio helps assess the efficiency of insurers’ business models and their ability to invest in technology, marketing, and customer service.

Regular tracking of these metrics ensures the sector remains competitive and responsive to evolving market conditions.

Emerging Industry Trends and Consumer Preferences

New trends shaping the industry include green insurance options, pay-as-you-go policies, bundling, cross-selling, and increased focus on underinsured markets and educational campaigns. Green insurance options are gaining traction, offering eco-friendly policies and incentives for renters in sustainable buildings. Flexible, pay-as-you-go policies now cater to those seeking short-term or nontraditional coverage, such as gig workers and frequent movers. Insurers are also bundling renters insurance with products like auto or pet insurance to streamline coverage and offer discounts. Cross-selling strategies target convenience-focused consumers, while educational campaigns and simplified policies are expanding access for underinsured markets, particularly among low-income renters and those in shared living spaces.

Technological Innovations and Digital Transformation

Technological advancements are rapidly transforming renters’ insurance, making products more personalized and efficient. AI-powered personalization enables insurers to tailor policies to individual lifestyles and risk profiles, ensuring renters pay only for the coverage they need. Smart home integration, such as security devices and leak detectors, not only enhances protection but can also lead to premium discounts for proactive risk management. Instant policy issuance through digital platforms streamlines the application process, allowing renters to secure coverage in minutes. Usage-based coverage models leverage real-time data to adjust premiums, offering greater flexibility and affordability for today’s diverse renter population.

Frequently Asked Questions

Renters face several risks that can result in significant financial loss if not properly insured. Below, we answer the most common questions about risks, claims, and the consequences of being uninsured or underinsured as a renter.

What are the most common risks renters face?

Theft, fire, water damage, and personal liability are the leading risks for renters. These events can cause loss of belongings, property damage, or legal responsibility for injuries to others.

How does renters’ insurance protect against theft?

Renters insurance can reimburse you for stolen personal property, up to your policy’s limit. This coverage helps replace your belongings if your apartment is burglarized or items are taken from your home.

Does renters’ insurance cover fire and water damage?

Yes, most policies cover damage to your personal property caused by fire, smoke, lightning, and certain types of water damage, such as burst pipes or accidental leaks from neighboring units.

What is personal liability coverage, and why is it important?

Personal liability coverage protects you if you’re held financially responsible for injuring someone or damaging their property. It covers legal costs, medical bills, or repairs, usually starting at $100,000.

What happens if I don’t have renters’ insurance?

Without renters insurance, you must pay out of pocket for lost property, repairs, or legal claims. This can lead to significant financial hardship after theft, fire, or liability incidents.

Are there coverage gaps renters should be aware of?

Yes. Standard policies may not cover certain events, high-value items, or damage caused by pets. Review your policy details and consider add-ons if you have special coverage needs.

Why do some renters remain uninsured or underinsured?

Many renters overestimate the cost of insurance or mistakenly believe their landlord’s policy covers their belongings. Others underestimate the risks or lack awareness about what renters’ insurance provides.

How can I avoid being underinsured?

Take inventory of your belongings and choose coverage limits that reflect their replacement value. Review your policy annually and update it as your living situation or possessions change.

What is the current market size of the renters’ insurance industry in 2025?

The U.S. renters insurance industry covers over 60 million policyholders, with market penetration reaching approximately 55% of all renters nationwide.

How much do renters typically pay for insurance in 2025?

The national average premium for renters insurance is around $170 per year, making it an affordable option for most renters compared to other types of insurance.

What are the main drivers of industry growth in 2025?

Growth is fueled by increased awareness, digital innovation, affordable pricing, and landlords’ increasing requirement for coverage as part of lease agreements.

Are there notable trends affecting the industry this year?

Yes, trends include expanded digital offerings, more flexible policy options, and a focus on improving accessibility for underinsured populations.

How does the industry outlook compare to previous years?

The industry is expected to expand steadily, with robust demand and new entrants driving competition and innovation in policy offerings and customer experience.

What challenges does the industry face in 2025?

Challenges include rising claims in disaster-prone regions, persistent misconceptions about coverage, and disparities in adoption among different demographic groups.

How does renters insurance adoption vary across the country?

Adoption rates are higher in states with lower premiums and greater awareness, while disaster-prone states with higher costs tend to see lower coverage rates.

Having the right renters’ insurance helps protect you from unexpected events and financial setbacks.