Credit Building With Rent Payments: How Reporting Rent Helps Tenants & Landlords

Discover how reporting rent boosts tenant credit scores, supports reliable payments, and strengthens landlord-tenant relationships.

Did you know more and more consumers are now using rent payments to boost their credit score?

Rent reporting lets renters build credit without taking on new debt, while giving landlords a simple way to encourage on-time payments and attract responsible tenants. With more tools making it easy to report rent to credit bureaus, this trend is picking up fast.

Rent payments are starting to carry real weight in credit histories, helping first-time buyers and renters improve their financial standing. Landlords benefit too, with more reliable tenants and smoother property management. Simply put, rent reporting is becoming a win-win for everyone in the rental market.

This page shares what you need to know about rent reporting to boost your credit score. As a landlord or property manager, read on to learn how this could help both you and your tenants.

What Is Rent Reporting?

Rent reporting is the process of sharing tenants’ rent payment history with the major credit bureaus. With this in place, you can help renters build or improve their credit scores simply by paying rent on time.

Essentially, this process allows rent as a regular, recurring expense to contribute to a tenant’s financial profile. It gives them access to better loans, credit cards, even housing opportunities. But as a property owner or manager, you can use rent reporting to encourage timely payments and attract responsible renters.

With digital tools making it easier than ever to report rent payments to credit bureaus, adoption is growing rapidly. More and more renters and landlords are turning to digital tools and credit-building services.

In fact, the rent reporting platform market could grow from $1.32 billion in 2024 to $3.86 billion by 2033 at a 12.6% compound annual growth rate (CAGR). This market growth and expansion are due to:

- Stronger demand for financial inclusion

- Smarter property management technology

- Regulatory support for alternative credit data

Rent reporting vs. standard credit-building tools

There are several ways to build credit. However, rent reporting stands out because it turns an existing monthly expense into a meaningful credit-building tool.

Unlike traditional methods, this doesn’t require taking on new debt or opening additional accounts, making it a practical choice for many renters.

That said, here’s how it compares to other common credit-building options:

- Credit-builder loans: These small loans are designed to establish a payment history. However, they require borrowing money and paying interest. This isn’t always ideal for renters already managing monthly expenses.

- Secured credit cards: While effective for building credit, they require a cash deposit and careful spending habits. That can be a barrier for some renters.

- Utility reporting: Paying utilities on time can help diversify a credit file, but not all utility providers report consistently to the credit bureaus. This limits its impact compared to rent reporting.

Tyler Denk, Co-founder and CEO of beehiiv, recommends leveraging technology for alternative credit reporting. He suggests using AI-powered platforms for rent reporting to boost property management efficiency and tenant credit scores.

Denk says, “Rent reporting is a game-changer for tenants and landlords alike. Using technology to automate reporting can encourage on-time payments while tenants build credit without taking on extra debt. It’s a simple way to create value for everyone involved.”

AI tools now track every rent payment in real time and flag issues before they disrupt cash flow. They highlight unusual patterns, missed dates, and changes in tenant behavior. Property teams act faster because the system shows exactly where attention is needed.

When owners use an AI ROI for enterprise lens, they focus on results: fewer late payments, fewer manual checks, and fewer hours lost on routine tasks. They see which tools protect revenue, cut admin work, and support stronger portfolio performance.

How Rent Reporting Benefits Both Tenants and Landlords

Rent reporting is gaining real momentum. According to TransUnion’s fourth annual Rent Payment Reporting analysis, the share of consumers having their rent data sent to credit agencies rose from 11% in 2024 to 13% in 2025.

This growth is expected to accelerate thanks to a new FHFA policy requiring Fannie Mae and Freddie Mac to accept VantageScore 4.0, which factors in rental payment history. With this shift, more renters (especially first-time buyers) could finally qualify for the mortgages they’ve been priced out of.

Most generations saw their participation in rent reporting rise, mirroring the overall upward trend. Gen Z was the only exception, dipping from 26% in 2024 to 18% in 2025; however, they still lead all age groups. With the shortest credit histories, this cohort stands to benefit the most from rent reporting’s ability to help them build credit faster.

But as a property owner or manager, why should you consider rent reporting? Here’s how it proves beneficial to both tenants and landlords:

For tenants:

Rent reporting gives tenants a simple way to strengthen their credit profiles using an expense they’re already paying: rent. As cited, it doesn’t require taking on new debt or opening extra accounts, making it a practical tool for renters at any stage of their financial journey.

That said, here’s how rent reporting benefits tenants or renters:

- It builds credit without taking on debts. On-time rent payments are reported directly to credit bureaus. These allow tenants to improve their credit scores without borrowing money or paying interest.

- It offers more predictable credit gains. Because rent is a regular monthly expense, tenants can steadily build credit score with rent payments. This creates a more reliable and transparent path to a stronger credit profile.

- It gives better access to loan opportunities. Higher credit scores open the door to financial products and/or services, such as mortgages and auto loans, that may have been out of reach before.

Take it from Andrew Bates, COO at Bates Electric. Having worked with various renters on electric services, he’s seen that rent reporting primarily benefits tenants.

Bates explains, “Rent reporting turns a routine monthly expense into real credit-building power. Tenants can improve their scores steadily without taking on new debt, giving them better financial opportunities and peace of mind.”

For landlords:

Rent reporting also offers tangible advantages for landlords and property managers.

While TransUnion’s latest findings show a slight dip in property manager participation, falling from 48% in 2024 to 44% in 2025, the overall trend highlights growing interest. This slowdown suggests that landlords may need clearer incentives or simpler tools to fully leverage rent reporting.

That said, here’s how rent reporting benefits property owners or managers:

- It attracts high-quality renters. Tenants who value credit-building opportunities tend to be more responsible and reliable. They help landlords reduce vacancy risk and turnover.

- It strengthens tenant-landlord relationships. Offering rent reporting demonstrates that you are invested in your tenants’ financial well-being. As a result, this fosters renters’ trust and long-term rental stability.

- It encourages on-time payments. By linking rent reporting to financial benefits, you can motivate tenants to pay promptly. You can even automate rent collection to reduce your administrative burden.

Learn from Travis Lambert, General Manager at Central Oregon Heating. Having worked with various landlords and property managers for HVAC services, he’s seen how rent reporting benefits them in more ways than one.

Lambert shares, “Rent reporting gives landlords a smarter way to manage properties. It encourages tenants to pay on time, strengthens relationships, and attracts renters who value responsibility. The result is smoother operations and fewer headaches for property owners.”

How To Implement Rent Reporting for Your Rental Business

Whether short, mid-, or long-term rentals, adding rent reporting to your property strategy can benefit both tenants and landlords. The process is straightforward, especially with modern digital tools designed to simplify reporting and track results.

As a property owner or manager, here’s how to set rent reporting in place:

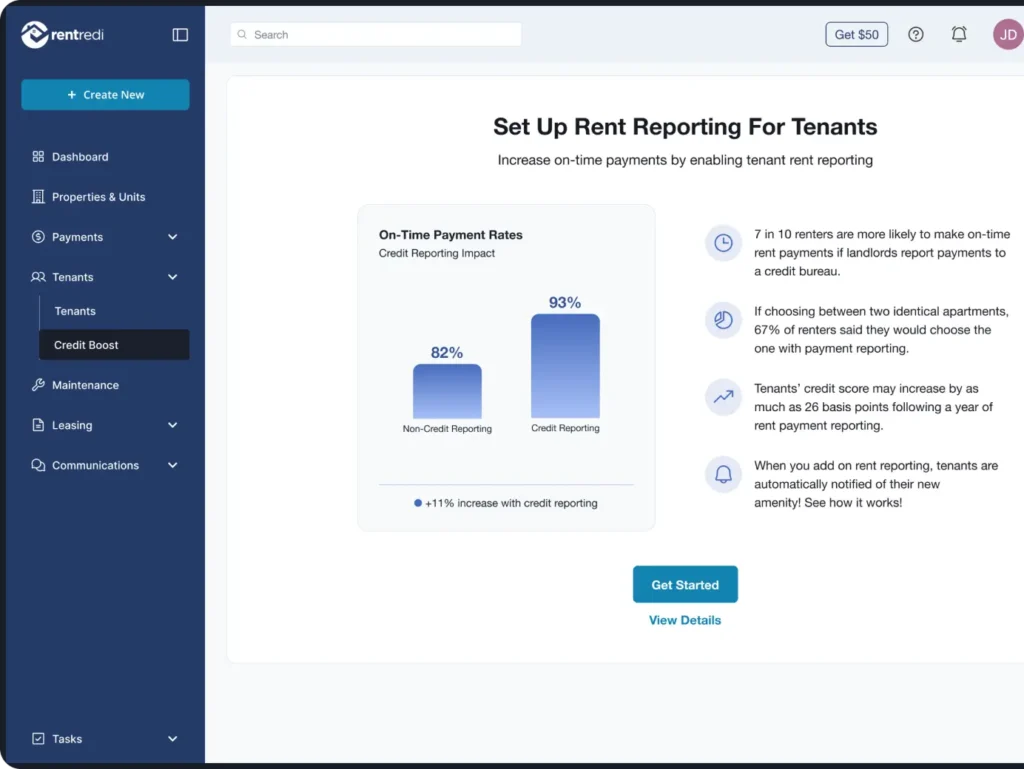

- Pick a rent reporting platform or service. RentRedi’s rent reporting feature boosts on-time rent payments and tenant credit scores. But while at it, choose a property management platform that lets you handle various rental functions, all in one place. This helps you save time and manage your properties more efficiently and effectively.

- Get tenant consent for rent reporting. Make sure each tenant agrees to have their rent reported to credit bureaus. Doing so keeps everything transparent and legally compliant. Clear communication about how their data will be used also helps build trust and encourages tenant participation.

- Set up your property and tenant details. Input accurate information for each unit and renter to ensure reporting is seamless. Key details typically include:

- Property information: Address, unit number, lease type (short-, mid-, or long-term), rental amount.

- Tenant information: Full legal name, date of birth, Social Security number or Tax ID (as required by the reporting platform), contact information, etc.

- Lease and payment terms: Move-in date, lease duration, payment schedule, and any late fee policies.

- Payment history setup: Include any prior on-time payments, if the platform allows. That way, tenants can receive credit for past rent.

- Secure and report monthly rent payments. Track payments consistently and report them to credit bureaus. Doing this regularly helps you monitor the top KPIs for your rental business, such as on-time payment rates and tenant credit improvements.

- Monitor credit reports and fix when needed. Keep an eye on tenants’ credit updates and resolve any discrepancies to maintain accuracy and trust. Regular monitoring ensures that all payments are being reported correctly and helps prevent errors from affecting tenants’ credit scores.

Todd Benadum, VP of Sales and Marketing at Elsco Transformers, suggests leveraging digital tools and technologies for rent reporting. They also tap into modern tech to boost accuracy, efficiency, even productivity.

Benadum mentions, “Digital platforms make rent reporting simple and effective. They help landlords track payments, report them accurately, and use the data to manage properties smarter. Technology turns a once-tedious task into a seamless part of property management.”

Final Words on Rent Reporting Benefits

Rent reporting is more than just a way for tenants to build credit. It’s a tool that strengthens tenant-landlord relationships.

For one, it encourages on-time payments among tenants while boosting their credit scores. On the flip side, it helps landlords and property managers run a smoother, more profitable rental business. Ultimately, it creates a win-win that benefits both renters and property owners!

Ready to make rent reporting work for your properties? Try RentRedi’s smart property management platform today to simplify reporting and boost tenant satisfaction, ultimately streamlining your overall rental operations. To learn more, sign up today!