KEY TAKEAWAYS

- RentRedi’s rent reporting feature, Credit Boost, allows tenants to report their on-time rent payments to credit bureaus and improve their credit scores.

- Credit Boost improves tenant quality by incentivizing tenants to make on-time payments more often.

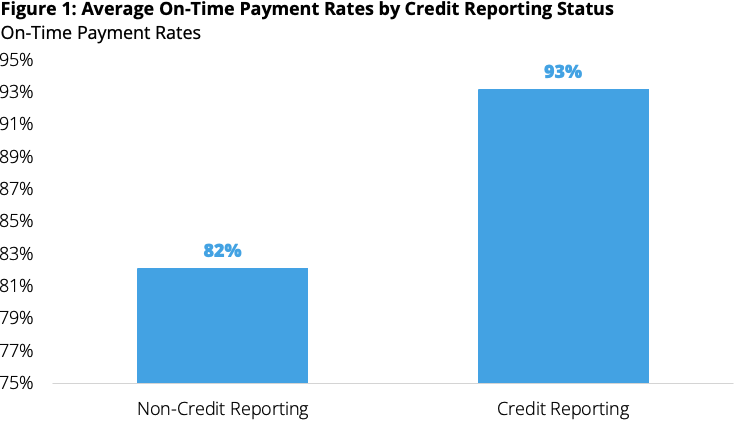

- On-time payments have averaged 93% for credit-boosting users, while non-credit-boosting users averaged 82% since January 2020.

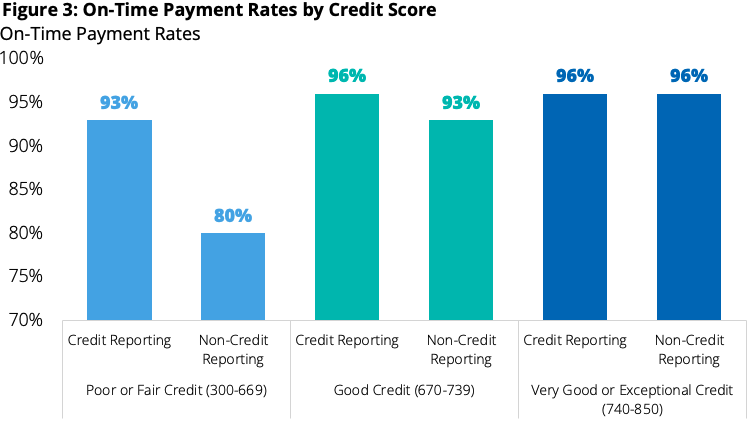

- When controlling for credit score ranges, on-time payment rates improve for those using credit boosting.

- Since January 2020, credit-boosting users with poor-to-fair credit scores paid 93% of their charges on time, while those without credit boosting paid on time around 80% of the time.

Property Management Software Provides Credit Boost

To more efficiently manage investment properties, real estate investors and landlords frequently use property technology (PropTech) called property management software. In addition to automating tasks such as payment collection, property listings, and tenant screening, PropTech also enables credit reporting.

Credit reporting is a feature that submits on-time rental payments made via property management software to major credit bureaus like Transunion, Equifax, and/or Experian.

Rent reporting is integral to the renting process, as its positive impacts can improve a tenant’s quality of life with better credit scores. Credit scores play a significant factor in loans, insurance, and securing home mortgages — all major points where a tenant’s financial health is critical when it comes to the renting experience.

Consequently, RentRedi developed a feature called Credit Boost that offers landlords and tenants add-on rent reporting. This allows tenants to report their on-time rent payments to credit bureaus like TransUnion, Experian, and Equifax to improve their credit scores. Before Proptech’s advancement, using rent to improve their credit scores would have been impractical at best—if not impossible. Reporting on-time rent payments can have a big impact helping people move closer to financial goals such as home ownership, car purchases, or even lower credit card interest rates.

With solid credit reporting adoption rates for tenants and robust payment adoption for landlords, RentRedi can see Credit Boost’s impact on the tenants’ on-time payment rates. Our analysis shows that landlords receive a clear benefit: Credit Boost improves tenant quality by incentivizing tenants to make on-time payments more often.

On-time payments have averaged 93% for credit-boosting users (Figure 1), while non-credit-boosting users averaged 82% since January 2020. Some evidence that consumer credit reporting interventions improve borrower performance exists in the economic literature. For example, research by Homonoff, Rourke O’Brien & Sussman (2021) suggests that student loan borrowers who were told their credit scores were available decreased their late payments and raised their scores.1

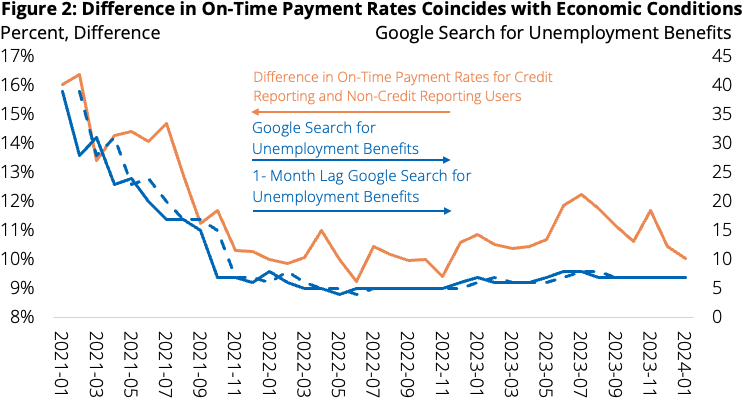

In 2021, the gap in on-time payment rates for credit and non-credit boosting users widened to over 16%, as shown in Figure 2. The larger-than-usual gap is likely related to the U.S. economy experiencing high levels of unemployment insurance filings during 2021 when initial unemployment claims averaged 459 thousand—a significant jump relative to the 2015-2019 monthly average (244k), according to FRED via the U.S. Employment and Training Administration. Prior work by Chandan Economics suggests that the overall on-time payment rate is related to monthly Google searches for unemployment insurance benefits.

As insurance claims aligned with its historical norm, the difference in on-time payment rates by credit boosting status also fell—hovering around 10.5% over the last two years.

When controlling for credit score ranges, on-time payment rates improve for those using credit boosting.

Generally, users with poor-to-fair credit scores may find it more difficult to obtain loans and pay higher interest rates. Since January 2020, credit-boosting users with poor-to-fair credit scores paid 93% of their charges on time, while those without credit boosting paid on time around 80% of the time as shown in Figure 3.

Not only does credit boosting improve on-time payment rates, but it also reduces unpaid rent charges. Only 2% of rent charges to credit-boosting users with poor-to-fair credit scores went unpaid—a similar rate to those with higher credit scores.

We see a slight improvement for those with good credit scores, with credit-boosting users paying on time 96% of the time vs. 93% for those without credit boosting. We see high rates of on-time payments for users with the highest credit scores regardless of credit-boosting usage.

Methodology

RentRedi used credit score entries provided by a tenant to landlords for applications and prequalifications. Sometimes, the tenant entered a score range instead of a singular number for a score. In these cases, RentRedi uses the midpoint of the range as a proxy for the credit score.

RentRedi then matched each user’s credit scores to their charges. RentRedi categorized each charge into a credit score band based on its lowest matching credit score. The credit score categories match Experian’s categorization. Though this is a more conservative approach, our analysis was consistent when categorizing charges by averaging credit scores or using the unit’s highest credit score.

Payment status categories (on-time, late, and unpaid) are from the same methodology used in the Chandan Economics Independent Landlord Rental Performance Report. Critical features of Chandan Economics’ methodology are:

- It only includes rent income charges.

- It only contains charges between $500 and $10,000.

- It removes units that are inactive for more than two months from the sample.

Citations

Tatiana Homonoff, Rourke O’Brien, Abigail B. Sussman; Does Knowing Your FICO Score Change Financial Behavior? Evidence from a Field Experiment with Student Loan Borrowers. The Review of Economics and Statistics 2021; 103 (2): 236–250. doi: https://doi.org/10.1162/rest_a_00888